Australia is rapidly becoming a hotspot for Fintech innovation, which make it an attractive market for any financial businesses that want to launch modern payment apps. With a strong regulatory system, a tech-savvy population, and rising demand for digital financial services, the region offers fertile ground for Fintech startups to grow.

The country’s focus on innovation has driven businesses to seek expert agencies for developing Fintech apps that simplify financial transactions and deliver smooth user experiences. These apps cater to a growing need for secure, efficient, and user-friendly financial tools in Australian market.

Moreover, Australia’s regulatory environment strikes the right balance between encouraging innovation and ensuring data security, creating favorable conditions for both new Fintech startups and established players to thrive.

In this blog, we’ll explore what makes a Fintech company, the advantages of starting one in Australia, creative ideas to consider, the latest technology trends, and the essential steps to bring your vision to life. We’ll also look at the common challenges in payment app development, and how to overcome them to build a secure, scalable, and successful product.

What is a Fintech Company?

A Fintech company is a business that delivers financial services primarily through technology, such as mobile apps, web platforms, or APIs. These companies disrupt traditional finance by improving accessibility, reducing costs, and offering faster, more personalized experiences.

Rather than being an official classification, “Fintech” is often used as a self-identifying term. As the industry evolves, the distinction between traditional banks and Fintech startups is becoming less clear. For example, banks in Australia now offer features like high-yield savings accounts and chat support, while some Australian Fintech firms provide traditional services such as loans and mortgages. This convergence shows how Payment apps and other Fintech innovations are reshaping the financial services landscape.

Benefits of Launching a Modern Payment App

In today’s fast-paced digital economy, businesses and consumers expect consistent, secure, and convenient ways to handle financial transactions. For Fintech startups, developing a modern payment app offers far more than traditional financial services, it will create more benefits for their business. Below are 5 key advantages that bring the most impact.

- Streamlining Financial Operations

Traditional financial processes are time-consuming and prone to errors, which make it harder for startups to focus on growth. However, with automation and Fintech tools, essential tasks like invoicing, payroll, bookkeeping, and tax compliance will be simplified. They will reduce mistakes and save valuable time. For Fintech businesses, launching a modern payment app or payment automation allows recurring processes to run smoothly while minimizing compliance risks. Additionally, digital payment systems and expense tracking solutions will improve cash flow visibility, which is critical in the early stages. These innovations help Australian Fintech companies to cut costs, boost efficiency, and maximize productivity, which are key advantages for lean teams with heavy workloads.

- Enhancing Access to Funding

Securing capital is one of the biggest challenges for Fintech startups. Traditional financing options can be slow and restrictive, while digital funding platforms, peer-to-peer lending, and equity crowdfunding provide faster, more flexible alternatives. For financial companies, these tools not only expand access to investors but also offer real-time performance data to strengthen fundraising efforts. By adopting these solutions, Australian Fintech startups can secure growth capital more efficiently and focus on scaling their products.

- Facilitating Financial Planning and Analysis

Data-driven decision-making is vital for the growth of any businesses, but, with a Fintech firms, it doesn’t require spending hours analyzing spreadsheets. For examples, today’s Australian Fintech solutions provide advanced financial planning tools and real-time insights into business health. Many platforms include smart KPIs that track progress toward strategic goals, update instantly, and even recommend actions to improve low-performing areas. For companies that own these tools, it will be easier to monitor financial performance, make quick, informed decisions, and stay agile in a competitive market.

- Simplifying International Payments and Transactions

When expanding globally, Australian Fintech startups have to face new challenges, especially in managing international transactions. According to a PayPal survey, 76% of e-commerce customers prefer paying in their local currency, so localized currency options are key to attracting global users. However, for a financial business, unified financial overview is very important. Luckily, Fintech platforms with multi-currency support make this easier by automatically converting payments to a base currency. These solutions help the business simplify cross-border transactions, attract more users, and keep payment apps efficient while enabling global expansion.

- Ensuring Data Security and Compliance

Financial data protection and regulatory requirements are essential to build trust for any financial startups. However, for a Fintech companies, there will be other advanced safeguards like encryption, multi-factor authentication, biometric verification, and fraud detection are also considered to keep transactions secure. On the other hand, it is easy to meet compliance by using existing frameworks that support PCI DSS, ISO 27001, and privacy laws such as Australia’s APP and Europe’s GDPR. By embedding strong security and compliance measures from the start, Australian Fintech businesses can reduce risks, protect customers, and establish a reliable foundation for growth.

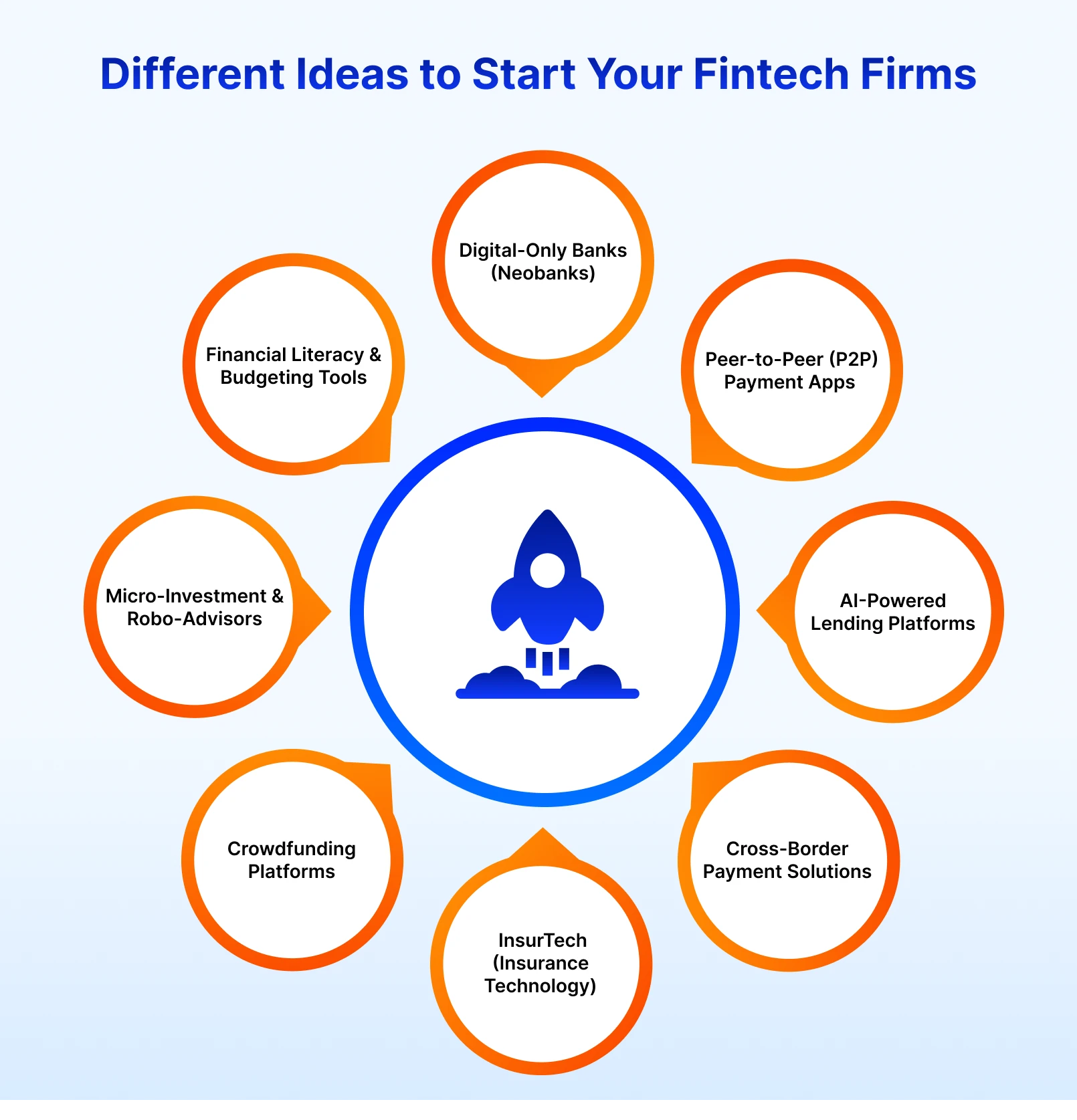

Ideas to Start Your Fintech Firms

If you’re planning to enter the Australian Fintech market, you’ll need a strong business idea that meets real customer needs. Here are some of the most promising concepts that reshape the industry today:

- Digital-Only Banks (Neobanks)

Neobanks operates entirely online without physical branches. They provide easy access to banking through modern payment apps, which offer features like instant transfers, budgeting tools, and low-fee accounts. This model appeals to tech-savvy customers who want convenience and transparency and help you save on rental costs.

Examples: Up Bank, Judo Bank, Ubank.

- Peer-to-Peer (P2P) Payment Apps

P2P payment apps allow users to send and receive money instantly, often with lower fees than traditional banks. By integrating social features and digital wallets, these platforms make transactions simple and fast.

Examples: Beem, PayID, PayPal.

- AI-Powered Lending Platforms

These platforms use AI and machine learning to assess creditworthiness quickly, automate approvals, and provide personalized loan offers. It’s an ideal niche for Fintech startups that aims to speed up lending processes while reducing risk.

Examples: LoanOptions.ai, Tiimely, Lendi.

- Cross-Border Payment Solutions

International payments can be slow and costly. Fintech startups can build modern payment apps that simplify cross-border transactions, lower fees, and ensure real-time currency conversions. This is especially relevant for Australian Fintech businesses targeting global markets.

Examples: Wise (TransferWise), Airwallex.

- InsurTech (Insurance Technology)

InsurTech companies modernize insurance by using AI for claims automation, risk analysis, and personalized pricing models. With growing demand for digital insurance solutions, this is a big opportunity for Fintech startups.

Examples: iSelect, Upcover, Cover Genius.

- Crowdfunding Platforms

These platforms let businesses or individuals raise funds from a large pool of investors, either for equity or rewards. This model has gained traction among startups and creative projects.

Examples: Mycause, Pozible, Equitise.

- Micro-Investment & Robo-Advisors

Investment apps that allow users to start investing with just a few dollars are trending. They often round up everyday purchases and invest the spare change. This concept is perfect for Fintech startups that focus on financial inclusion.

Examples: CommSec Pocket, Spaceship Voyager, Raiz (popular in Australia).

- Financial Literacy & Budgeting Tools

With rising demand for financial wellness, budgeting tools that integrate with banking and payment apps can help users track spending, save money, and make smarter financial decisions.

Examples: Beem, Frollo.

- BNPL (Buy Now, Pay Later) Services

BNPL solutions let customers purchase items and pay later in installments. This model is booming in Australian Fintech, with companies like Afterpay leading the charge.

- Cryptocurrency & Digital Assets Platforms

Crypto exchanges, wallets, and DeFi solutions continue to attract more attention. Building Fintech app that supports crypto transactions can help your Fintech startup stand out.

Key Technology Trends When Creating a Modern Payment App

Fintech sector is moving at lightning speed, and technology is the core of this transformation. For startups and established players, staying update of emerging trends is crucial to building payment apps that are secure, scalable, and user-friendly. From artificial intelligence and Blockchain to cloud computing and open banking, these solutions are shaping how financial services are delivered in Australia and worldwide. Below are the key technology trends every Fintech company should consider when creating a modern payment app.

- Artificial Intelligence (AI) & Machine Learning

AI is no longer just a trend, it’s a game-changer for Fintech startups and even big players in Australian Fintech market. From detecting fraud instantly to offering personalized loan recommendations, AI also powers everything from chatbots to automated credit scoring in modern payment apps.

- Blockchain & Distributed Ledger Technology

Blockchain is redefining financial services far beyond cryptocurrency. Many payment apps now use blockchain to make transactions faster, cheaper, and more secure. For Fintech startups worldwide in general, and in Australia in particular, this technology ensures transparency and trust in every transaction.

- Cloud Computing

When building a payment app, scalability is key. So, cloud computing is a good choice to help Fintech startups grow without heavy infrastructure costs. It also improve real-time payment speed and global accessibility, which is crucial for companies that aim to compete in the Australian Fintech landscape.

- API-First Architecture & Open Banking

Open banking is a massive opportunity for Fintech startups that want to quickly grow up in Australian market. Its APIs make it easy to connect with banks, payment apps, and third-party services, enabling features like account aggregation and embedded finance in modern payment apps.

- Cybersecurity & Data Privacy

Security is a non-negotiable thing for Fintech startups. There are some security methods such as multi-factor authentication, biometric logins, and real-time fraud detection that ensure customers trust your solution. This is critical for any Australian Fintech company that handles sensitive data.

- RegTech (Regulatory Technology)

Regulatory compliance is complex, but RegTech simplifies it for Fintech startups. For example, automated KYC and AML checks reduce costs and errors, which helps payment apps stay compliant in strict financial environments like Australian Fintech Market.

- Big Data & Advanced Analytics

Data-driven insights power smarter decisions for Fintech startups. Whether you’re building a payment app or a lending platform, big data helps personalize user experiences and predict future trends. In Australian Market, this is a competitive advantage that Fintech startups must have.

- Real-Time Payments & Digital Wallets

Consumers always expect instant transactions. Payment apps are leading this shift with real-time payments and digital wallets, which improve convenience and user trust. For an Australian Fintech startup, speed is a key competitive advantage, the faster the payments, the more users it will attract.

- Quantum Computing (The Future)

While not mainstream yet, quantum computing promises ultra-secure encryption and faster processing for Fintech startups. It could change everything from fraud detection to real-time analytics in payment apps of the future.

- Embedded Finance

Embedded finance is about integrating financial services into another app. Let’s think about taxi booking apps that integrate financial features of your payment app, it will enhance user experience for the booking app, and your payment app also have more users. For Australian Fintech companies, this trend opens new ways to add value and keep customers engaged.

7 Essential Steps to Launch Your Fintech Company

Starting a Fintech company is an exciting but challenging journey, especially in a fast-moving market like Australia. To succeed, you need more than just a great idea, you need a clear roadmap that takes you from research to launch. Each step, from validating your concept and building an MVP to ensuring compliance and choosing the right technology, plays a crucial role in shaping your success. Below, we’ll walk through seven essential steps that will guide you in developing a modern payment app and positioning your Fintech startup for long-term growth.

- Conduct Market Research

Before starting a Fintech startup, you should conduct detailed market research which involves analyzing industry trends, identifying customer pain points, and studying competitors. When you understand your target audience’s expectations and evaluate existing payment apps, you can discover opportunities to differentiate your product. For Australian Fintech businesses, this step validates their idea and ensures their solution meets real market needs. This research will form the foundation for developing a competitive product and achieving long-term success.

- Define your minimum viable product (MVP)

Once your research is complete, the next step for any Fintech startup is product development. Let’s start by prioritizing features that solve the core problem and align with your business goals. The best approach is to build a Minimum Viable Product (MVP) – a version containing only essential functionalities to validate your idea. For Australian Fintech startups, an MVP helps test the product with real users, gather feedback, and make improvements before scaling to a full release. This approach minimizes risk, saves costs, and ensures your payment app meets user expectations.

- Ensure Legal and Regulatory Compliance

Regulatory compliance is one of the most critical aspects of running a Fintech startup. The financial industry is governed by strict regulations, so your business must meet all legal requirements. This includes obtaining the necessary licenses, adhering to Anti-Money Laundering (AML) and Know Your Customer (KYC) standards, and ensuring data protection in line with regulations like GDPR. So, for any Australian Fintech company, compliance is non-negotiable. To manage this complex process, you can consider partnering with legal experts who can help you navigate regulations and maintain compliance as your business scales.

- Select the right Technology Stack

Choosing the right technology stack is one of the most important decisions for any Fintech startup. The tech stack will define the scalability, security, and performance of your financial solutions. It needs to handle complex transactions and large data volumes efficiently. A strong foundation usually includes:

- Backend: You can consider languages like Python, Java, or Node.js to build reliable, scalable applications.

- Frontend: There are some frameworks such as React.js or Vue.js that help you create smooth and responsive user experiences.

- Database: You can use PostgreSQL or MongoDB for efficient data storage.

- Cloud Services: Some platforms like AWS, Google Cloud, or Microsoft Azure can help your Fintech app more flexibility and scalability.

- Security: Let’s apply advanced encryption and authentication methods like OAuth or JSON Web Token to keep your payment apps secure.

For any Australian Fintech business, the tech stack is the backbone, so let’s select programing language and frameworks that support long-term growth and innovation.

- Assemble a professional team

It is really important to build a strong team for any Fintech startup. Your team should include specialists in finance, technology, compliance, and marketing to ensure all aspects of your Fintech business are covered. A well-rounded group will help you bring new ideas, solve complex challenges, and accelerate growth. When you hire or prioritize candidates with experience in payment app development or those passionate about Fintech innovation. Your team will not only drive product development but also keep your payment apps competitive in a fast-evolving market.

- Develop your Fintech Product

After assembling your team, you’ll need to decide on a development approach, there are two ways for you to consider:

- In-House Development: With this method, you will create your product from the ground up, which offers full control and flexibility, and makes it ideal if you need unique features. However, you have to invest significant time and resources.

- Using Ready-Made Solutions: You can consider integrating pre-built platforms or Fintech software into your Fintech app to speed up your launch and reduce costs. This approach lets you focus on customization and important features rather than building every element from scratch.

Each method has its advantages and trade-offs, so choose the one that best fits your budget, timeline, and product goals.

- Testing and Launch

Once your product is fully developed and tested, it’s time to launch. Let’s begin with a pilot launch to gather insights from early users and refine the product based on their feedback. After adjustments, you can move forward with a full-scale rollout to approach the full Australian market.

To attract more users, you have to focus on targeted marketing, partnerships with influencers, and creating engaging user experiences. When you have a stable number of users, let’s keep monitoring feedback, improving features, and try to explore new markets. Your long-term success will depend on continuous innovation and adapting to evolving customer needs.

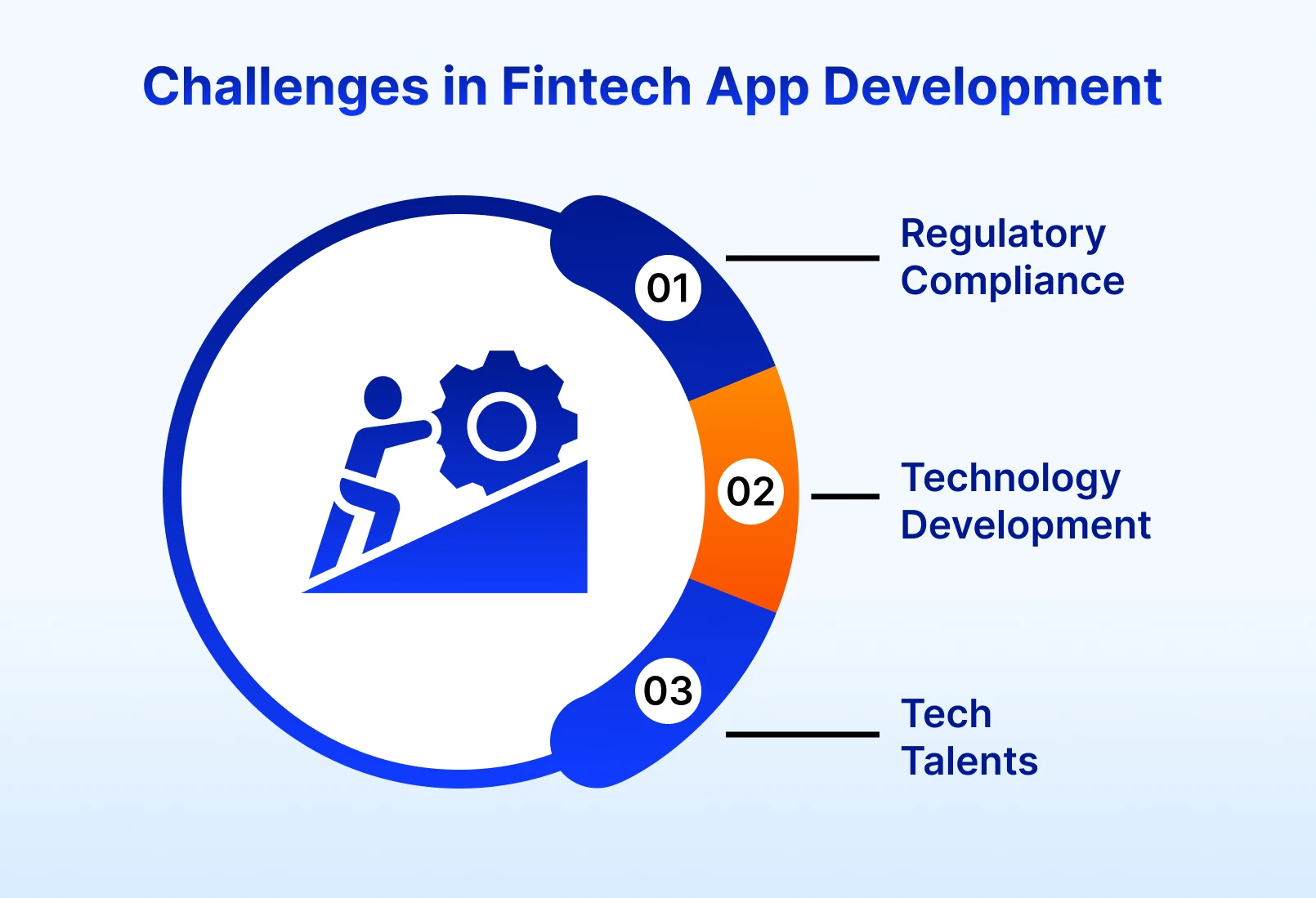

Challenges in Fintech App Development

Starting a Fintech startup comes with a variety of financial challenges. From product development to marketing and scaling, it is very important to understand the cost breakdown for proper planning and resource allocation. Overall, the expenses can change depending on the size of your business and the development method you choose. Below are 3 key areas you need to consider the cost carefully when building a modern payment app for the Australia market.

- Technology development

This cost can vary widely based on your chosen tech stack and team structure. Major factors to account for include:

- Development Expenses: It covers both front-end and back-end coding, API integrations, security implementation, and continuous maintenance.

- Infrastructure and Hosting: This involves servers, cloud platforms, databases, and storage solutions from providers like AWS, Google Cloud, or Azure.

- Payment Gateway Setup: This cost will be counted when you configure systems to handle transactions, whether through credit cards, digital wallets, or Blockchain-based payment methods using payment gateways such as Stripe or PayPal.

- Regulatory Compliance

Managing regulatory requirements in Fintech often involves significant investment in legal expertise and compliance tools to meet financial standards.

- Licensing Fees: Costs associated with securing necessary financial licenses based on your operating region, such as money transmitter permits or investment advisory registration.

- Compliance Expenses: Covering adherence to local and global regulations like GDPR, PSD2, AML, and KYC.

- Legal Services: Engaging legal professionals to handle complex regulations, draft contracts, and ensure all documentation aligns with industry standards.

- Tech Talents

Building a Fintech app requires significant investment in many roles such as developers, QC, QA, project manager, UX/UI designer…

For software development, you can choose between two main options:

- In-House Team: This option offers full control, faster decision-making, and strong alignment with company goals. However, it demands higher upfront costs, including salaries, infrastructure, and long-term commitments.

- IT Outsourcing: A more cost-efficient choice for projects which need specialized skills, tight development timeline, flexibility in scale up and down. And the most important thing, it provides access to global talent at lower costs.

Additionally, other areas, such as marketing and customer engagement, also involve expenses for paid ads, social media, SEO, influencer partnerships, and tools or staff to manage customer support systems effectively.

Conclusion

Australia’s Fintech ecosystem is evolving rapidly, driven by growing demand for secure and user-friendly payment apps alongside a regulatory environment that supports both innovation and compliance. For Fintech startups, the opportunity is not just in creating the next modern payment app, but in building trust, scalability, and seamless user experiences that customers can rely on.

At LARION, we empower Australian Fintech companies to turn bold ideas into market-ready products. With proven expertise in software development, compliance-focused solutions, and scalable infrastructure, we help Fintech startups accelerate innovation while keeping data security at the core.